|

|

As an option trader, one notes that most of the time the market or stock prices dont move much within a small period of time. Rather they trace back to the same levels even if there is a slight movement upwards or downwards. Can we take benefit of such limited range price movements? The answer is YES and that's where the SHORT STRADDLE option trading comes to the picture.

Let's see the details and in-depth analysis of Short Straddle Trading in this series of articles:

What is a Short Straddle Option Trading?

A Short Straddle Option Position is a net SELL (also called net SHORT) option position where the option trader Shorts 2 options - 1 ATM Call and 1 ATM Put Option. Since there are 2 sells, it is a net credit position which means that the option trader receives option premium (net inflow) while getting into the trade. However, please note that since there is shorting of options, the trader might be required to keep margin money with the options broker and this margin money amount can be considerably higher than the net option premium received which means that in summary this Short Straddle position is actually a net debit position.

Also note that usually since the ATM call & put are bought, which are known to have the highest time decay value, the net price or option premium received is usually high.

In which scenarios is the Short Straddle Option Trading profitable to the trader?

A trader should take the Short Straddle Option Trading position only when he/she is expecting the underlying price to remain confined to a certain range - near the current market price (hence the ATM call and put selection).

That means a SHORT STRADDLE should not be traded when big events or big news are expected - like company declaring quarterly results, expecting to get a big project and so on. Ideal scenario to trade short straddle will be when the stock is not expected to have any price movements.

For e.g., let's say MICROSOFT INC (MSFT) is trading at around $50 per share (the underlying stock price). There is nothing expected to happen to this stock/company - no news of earnings report, no outcome of any lawsuits, no problems from competitors, etc. Hence, the stock price is expected to stay around $50.

Hence, the above case for Microsoft makes it an ideal scenario for an option trader to get into a Short Straddle Option position.

Also note that since there are 2 shorts, the short straddle option trader will expect to benefit from time decay. Since time decay is fastest in the last month, take the short straddle position when there is at the maximum one month left for expiry. (See Options Time Decay: Explained with Examples)

If you don't want Short Straddle - then there is a similar scenario option trading position which the option trader can take Short Gut Options Trading: Example

Want to trade in a reverse scenario where a big price movement is expected? Go for Long Straddle Options Trading Explained: Example

How to construct the Short Straddle Option Trading position?

A Short Straddle Option Trading position can be constructed or configured by simply selling the SAME strike, SAME expiry Call & Put Options on the same underlying stock or index.

Usually, the strike price selected is ATM (at-the-money) strike price i.e. closest possible to current spot price. (Want to know what is ITM, OTM, ATM in Options? See Moneyness of Options - OTM, ATM, ITM Options)

1) 1 * ATM Short Put

2) 1 * ATM Short Call

Theoretically, here is how it looks:

An example of Short Straddle Option Trading

Suppose the Microsoft stock price is currently trading at $50 per share (just an example). You know that this stock may not move much in the next one month of expiry and is expected to stay somewhere around the current price of $50. Hence, you take the following positions for creating a Short Straddle Option Trading.1) Short Put with ATM strike price of $50 sold at the price of $5 &

2) Short Call with ATM strike price of $50 sold at the price of $5

Since there are 2 shorts, the total price or option premium you receive is $5 + $5 = $10 (net credit).

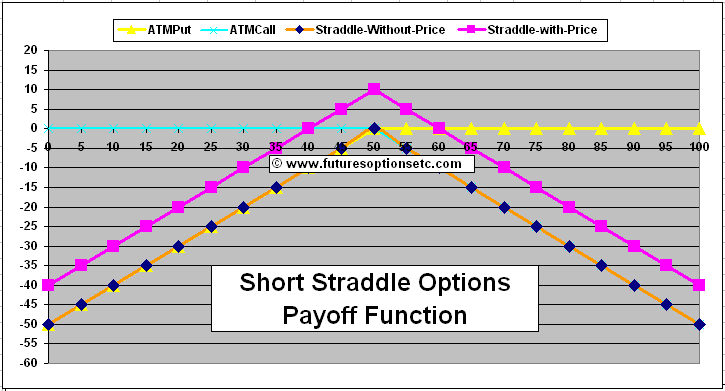

Payoff function for Short Straddle Option Trading

Here is the payoff function for Short Straddle Option without the price being considered:

Now, let's add them up together to get the NET ORANGE colored payoff function of Short Straddle Option - note that price is still not considered:

Finally, let's make the adjustment for the net price of $10 you paid to construct this Short Straddle Option and here we get the PINK colored final net payoff function for Short Straddle Option with price factored in:

Check out the same in the Video Tutorial-Short Straddle Option Trading Explained

Let's head on to next part Profit & Loss Calculations for Short Straddle Options Trading

0 Comments: Post your Comments

Wish you all profitable derivatives trading and investing activities with safety! = = Post a Comment